Is there an income limit for EV tax credit

EV Tax Credit 2024: Rules and Qualifications for Electric Vehicle Purchases

People who buy new electric vehicles may be eligible for a tax credit as high as $7,500, and used electric car buyers may qualify for up to $4,000 in tax breaks.

New this year, consumers can choose between claiming a nonrefundable credit on their tax returns or transferring the credit to the dealer to lower the price of the car at the point of sale, giving taxpayers more flexibility in how to apply the benefit.

However, there may be some hiccups for consumers as the changes roll out. Fewer cars are qualifying for the benefit in 2024 than previously, as battery manufacturing restrictions tighten.

Simple tax filing with a $50 flat fee for every scenario

With NerdWallet Taxes powered by Column Tax, registered NerdWallet members pay one fee, regardless of your tax situation. Plus, you'll get free support from tax experts. Sign up for access today.

for a NerdWallet account

Transparent pricing

Hassle-free tax filing* is $50 for all tax situations no hidden costs or fees.

Maximum refund guaranteed

Get every dollar you deserve* when you file with this tax product, powered by Column Tax.

Faster filing

File up to 2x faster than traditional options.* Get your refund, and get on with your life.

*guaranteed by Column Tax

What is the electric vehicle tax credit?

The electric vehicle tax credit, or the EV credit, is a nonrefundable tax credit offered to taxpayers who purchase qualifying electric vehicles or plug-in hybrid vehicles. Nonrefundable tax credits lower your tax liability by the corresponding credit amount but do not result in a refund of any excess credit amount.

In 2024, taxpayers can choose to either claim the tax credit on their federal returns or transfer the credit to an eligible dealership. For those who choose to transfer the credit, participating dealerships would then be able to either lower the cost of the vehicle by the corresponding credit amount or provide the consumer with a cash equivalent.

To qualify for either option, your income must fall beneath certain thresholds, and the vehicle you plan to purchase must also meet several IRS specifications, including price caps and manufacturing guidelines.

Which cars qualify for a federal EV tax credit?

As of April 2024, the following fully electric and plug-in hybrid vehicles may be eligible for either a full or partial tax credit if delivered on or after Jan. 1, 2024.

The IRS urges taxpayers to use the tool on the FuelEconomy.gov website for the most up-to-date information on eligible models. You can filter by purchase scenario, model year, and vehicle type and determine which car is eligible based on its date of delivery. Be sure to check with the dealer as well, the IRS warns, because some versions of the cars below may not qualify.

Q5 PHEV 55 TFSI e quattro (2023-2024)Q5 S Line 55 TFSI e quattro (2023-2024) |

Bolt (2022-2023)Bolt EUV (2022-2023) |

Pacifica PHEV (2022-2024) |

F-150 Lightning: Standard, Extended Range Battery (2022-2024) |

Grand Cherokee PHEV 4xe (2022-2024) |

Wrangler PHEV 4xe (2022-2024) |

Corsair Grand Touring (2022-2024) |

Leaf S (2024)Leaf SV Plus (2024) |

R1S Dual Large (2023-2024)R1S Quad Large (2022-2024)R1T Dual Large (2023-2024)R1T Dual Max (2023-2024)R1T Quad Large (2022-2024) |

Model 3 Performance (2023-2024) |

Model X Long Range (2023-2024) |

Model Y AWD (2023-2024)Model Y Performance (2023-2024)Model Y RWD (2024) |

ID.4 AWD ProID.4 AWD Pro SID.4 AWD Pro S Plus ID.4 ProID.4 Pro SID.4 Pro S Plus |

How to qualify for the 2024 EV tax credit

Price cap

Vans, SUVs and pickup trucks must have an MSRP, or manufacturer's suggested retail price, of $80,000 or less to qualify. Other vehicles, such as sedans and passenger cars, are capped at $55,000. For used vehicles, the price cap drops to $25,000.

For new vehicles, the MSRP, as defined by the IRS, is the base retail price provided by the manufacturer, plus the retail price of each accessory or optional piece of equipment that is physically present on the car at the time of delivery to the dealer. For purposes of claiming the credit, MSRP does not include taxes and other fees added on by the dealer.

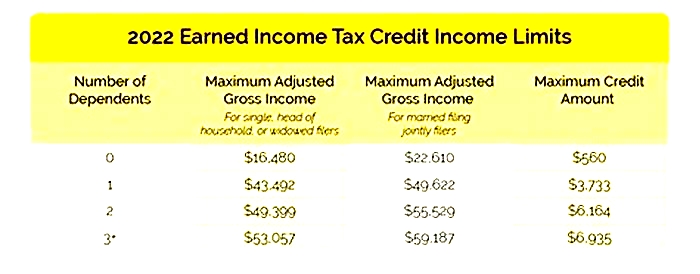

EV tax credit income limits

New EVs

Single and married filing separately: $150,000.

Head of household: $225,000.

Married filing jointly: $300,000.

Used EVs

Single and married filing separately: $75,000.

Head of household: $112,500.

Married filing jointly: $150,000.

A nice bonus here is that, per the IRS, you can use your MAGI from either the year the car is delivered, or the year before delivery. This means if your income exceeded the threshold one year, but was below the cap during the other year, you may still be able to snag a credit.

If your income precludes you from qualifying, there are also several tax strategies you can consider to lower your income throughout the year, such as maxing out your 401(k) or contributing to an HSA or FSA.

Final assembly requirements

To be eligible for the credit, vehicles must have had final assembly in North America. You can reference the National Highway Traffic Safety Administrations VIN, or vehicle identification number, database to check out a cars final assembly details.

Used EV tax credit qualifications

Qualifying used EV purchases can fetch taxpayers a credit of up to $4,000, limited to 30% of the cars purchase price. Some other qualifications:

Used car must be plug-in electric or fuel cell with at least 7 kilowatt hours of battery capacity.

Only qualifies for the first transfer of a vehicle.

Purchase price of car must be $25,000 or less.

Car model must be at least two years old.

Vehicle must weigh less than 14,000 pounds.

Credit can only be claimed once every three years.

Simple tax filing with a $50 flat fee for every scenario

With NerdWallet Taxes powered by Column Tax, registered NerdWallet members pay one fee, regardless of your tax situation. Plus, you'll get free support from tax experts. Sign up for access today.

for a NerdWallet account

How the electric vehicle tax credit is calculated

The new tax credit, worth up to $7,500, consists of battery and sourcing requirements, each adding up to half of the credit. If the car meets both requirements, it is eligible for the full credit. If it meets only one requirement, it may be eligible for a partial credit of $3,750.

Per the IRS, the requirements below apply to vehicles that are delivered (i.e., placed in service) to the taxpayer on and after April 18, 2023.

To be eligible for the battery portion of the credit (up to $3,750), a certain percentage of the vehicles battery must be assembled or manufactured within North America. The percentage thresholds will be as follows:

Critical minerals requirement

Cars must meet a "critical minerals requirement" to receive the remaining $3,750 portion of the credit. This requirement stipulates that a certain percentage of critical minerals in the car's battery must be extracted or processed within the U.S. or within a country with which the U.S. has a free-trade agreement. The percentage thresholds will be as follows:

Beginning in 2024, vehicles may also not source battery parts from a foreign country of concern (e.g., China). And starting in 2025, EVs cannot contain any critical minerals sourced from a foreign country of concern.

How to claim the federal EV tax credit

Claiming the clean vehicle tax credit on your taxes

To claim the credit, taxpayers can file Form 8936 when they file their federal income taxes. The credit is nonrefundable, which means it can lower or eliminate your tax liability, but you won't get any overage of the credit refunded once your liability hits zero. You also won't be able to carry over any excess amount to offset future taxes.

Some fine print: According to the agency, you generally can only claim the clean vehicle tax credit for the tax year the vehicle was delivered to you, not necessarily the year it was purchased. This means, for example, that if you bought a qualifying EV in 2023 but won't receive it until 2024, you must claim the credit on your 2024 tax return (filed in 2025).

Transferring the EV tax credit to a dealer

Taxpayers who transfer the credit to the dealership for a direct discount still need to follow a few tax rules. Transferring can result in an immediate discount on your purchase rather than a reduction in your tax liability when you file the following year. However, it does not do away with having to report your purchase on your taxes.

If you transfer the EV credit to the dealer, youll also need to fill out Form 8936 when you file your return for that year to report on your election and to provide the agency with your VIN. And buyer beware if you take a rebate but are not eligible for it, youll be required to pay the IRS back when you file your tax return.

What information do you need to claim the EV tax credit?

Before you leave a dealership with a new EV, make sure you have certain documents that youll need to claim the credit or report the purchase on your taxes.

If youre claiming the credit on your tax return

Sellers must provide taxpayers with a report containing certain information about the vehicle and this report should be furnished to the taxpayer by the date of the vehicles purchase. Make sure it includes the following:

If youre transferring the credit to the dealer

If youre electing to transfer the credit to the dealer for a direct discount, you must disclose your taxpayer identification number typically your Social Security number and a photo ID at the time of purchase:

You must also officially attest to, or confirm, the following information:

EV rebates and incentives

With all the focus on credits, its important to know about additional incentives on the state and local levels. Californias Clean Air Vehicle program, for example, grants carpool lane access to select electric vehicles. And New Yorkers might be eligible for a state-level rebate of up to $2,000 on top of the federal tax credit.

Make sure youre aware of any restrictions that come with applying for multiple incentives, though. Some states may not allow you to double-dip or claim a state-level rebate on top of a federal one.

Leasing and the EV tax credit

Although individual consumers cant claim the clean vehicle tax credit when leasing an EV, they might still see some trickle-down savings passed down from the dealer if they choose to lease.

Some businesses (i.e., dealerships and leasing agencies) may qualify for another type of tax credit called the commercial vehicle tax credit. The commercial credit is far less restrictive than the clean vehicle credit currently available to individual taxpayers. It allows businesses to claim tax breaks for a wider range of eligible electric vehicles, including ones that were not manufactured in the U.S.

Even though the dealership gets the tax credit for purchasing the car, the potential benefit to individual consumers here is that the dealer can, in theory, then pass down the savings by lowering the leasing cost by the credit amount.

A word of caution for potential lessees, though: Just because the dealership could pass those savings onto you, doesnt mean it will. Dealers arent required to give customers a discount on their leases, so it may require some negotiating on your end.

Assessing the transparency of any deal that claims the savings are being passed down may also require research and shopping around to ensure youre getting the best deal. Plus, there are other factors about leasing that you may want to take into account.

The clean vehicle credit expansion is exciting news for taxpayers looking to go green, but it still remains fairly complicated and nuanced especially given the murk surrounding the new sourcing requirements that are set to adjust each year. If youre confused about your eligibility or want guidance for your personal situation, consider consulting a qualified tax professional, such as a CPA or a tax preparer, before you sign on the dotted line.

Topic B Frequently asked questions about income and price limitations for the New Clean Vehicle Credit

Updated FAQs were released to the public in Fact Sheet 2024-14PDF, April 2024.

The Inflation Reduction Act of 2022 (IRA) makes several changes to the tax credit provided in 30D of the Internal Revenue Code (Code) for qualified plug-in electric drive motor vehicles, including adding fuel cell vehicles to the 30D tax credit. The IRA also added a new credit for previously owned clean vehicles under 25E of the Code.

These FAQs provide detail on how the IRA revises the credit available under 30D (New Clean Vehicle Credit) for individuals and businesses, and information on the credit available under 25E (Previously Owned Clean Vehicle Credit) for individuals, and the new credit for qualified commercial clean vehicles under 45W of the Code.

Q1. Could my income level prevent me from taking the New Clean Vehicle Credit? (updated Oct. 6, 2023)

A1. Yes. You may not claim the credit if your modified adjusted gross income (AGI) exceeds certain thresholds. This limitation is based on the lesser of your modified AGI for the year that the new clean vehicle was placed in service or for the preceding year. The relevant modified AGI thresholds are as follows:

- Married filing jointly or filing as a qualifying surviving spouse or a qualifying widow(er) - $300,000

- Head of household - $225,000

- All other taxpayers - $150,000

Your modified AGI is the amount from line 11 of your Form 1040 plus:

- Any amount on line 45 or line 50 of Form 2555, Foreign Earned Income.

- Any amount excluded from gross income because it was received from sources in Puerto Rico or American Samoa.

If your filing status changes between the preceding year and the current year, you may claim the New Clean Vehicle Credit if your modified AGI is less than or equal to the threshold applicable to your filing status for in the preceding year or current year.

Q2. How do the income thresholds apply to my partnership's purchase and use of a new clean vehicle? (added March 31, 2023)

A2. If a partnership or an S corporation places a new clean vehicle in service and the New Clean Vehicle Credit is claimed by individuals who are direct or indirect partners of that partnership or shareholders of that S corporation, the modified AGI thresholds apply to those partners or shareholders.

Q3. Are there any price limitations on new clean vehicles eligible for the credit? (updated Oct. 6, 2023)

A2. Yes. The manufacturer's suggested retail price (MSRP) for the new clean vehicle may not exceed the following amounts for the following vehicle types:

- Vans - $80,000

- Sport utility vehicles - $80,000

- Pickup trucks - $80,000

- Other - $55,000

If the MSRP exceeds the limitation for that specific vehicle type, that vehicle is not eligible for the New Clean Vehicle Credit.

The Department of Energy hosts a purchaser-friendly version of IRS's list of eligible clean vehicles, including battery electric, plug-in hybrid and fuel cell vehicles, that qualified manufacturers have indicated to the IRS meet the requirements to claim the New Clean Vehicle Credit on FuelEconomy.gov, including the applicable MSRP limitation.

Q4. How will I know what the MSRP is for a vehicle? (added Dec. 29, 2022)

A4. The MSRP will be on the vehicle information label attached to each vehicle on a dealer's premises. The MSRP for this purpose is the base retail price suggested by the manufacturer plus the retail price suggested by the manufacturer for each accessory or item of optional equipment physically attached to the vehicle at the time of delivery to the dealer. It does not include destination charges or optional items added by the dealer, or taxes and fees.

Q5. Would I still qualify for the New Clean Vehicle Credit if the purchase price, including sales tax, fees, negative equity on a trade, etc., exceeds the MSRP threshold? (added Dec. 29, 2022)

A5. The credit limitations on the price of the vehicle are based on MSRP, not the actual price you paid for the vehicle. See Topic B FAQ 3 for how to determine the manufacturer's suggested retail price.

Q6. If the manufacturer/dealer offers incentives on the purchase, and the total purchase price drops below the MSRP limitation, will the vehicle be eligible for the new clean vehicles credit? (added Dec. 29, 2022)

A6. The credit limitations on the price of the vehicle are based on MSRP, not the actual price you paid for the vehicle. See Topic B FAQ 3 for how to determine MSRP.

Q7. How do I know if my vehicle is a pickup truck, van, sport utility vehicle (SUV) or other type of vehicle for purposes of determining the applicable MSRP for a vehicle? (updated Oct. 6, 2023)

A7. A vehicle's classification for this purpose relates to the classification describing the vehicle on the fuel economy label included as part of the window sticker as well as the EPA Size class displayed on FuelEconomy.gov. Vehicles whose class includes "sport utility vehicle," "pickup truck" or "van" on the fuel economy label or on FuelEconomy.gov are considered a sport utility vehicle, pickup truck or van respectively for this purpose, and the $80,000 MSRP limit applies, including for the following vehicle classes:

- Small sport utility vehicle

- Standard sport utility vehicle

- Small pickup truck

- Standard pickup truck

- Minivan

- Van

If your eligible vehicle is not in one of the classes described in the list above, the $55,000 MSRP limitation applies.

The Department of Energy hosts a purchaser-friendly version of IRS's list of eligible clean vehicles, including battery electric, plug-in hybrid and fuel cell vehicles, that qualified manufacturers have indicated to the IRS meet the requirements to claim the New Clean Vehicle Credit on FuelEconomy.gov, including the applicable MSRP limitation.

Q8. If my vehicle's classification changed since it was purchased, can I claim the New Clean Vehicle Credit? (updated Oct. 6, 2023)

A8. Eligible taxpayers who placed in service an eligible vehicle on or after Jan. 1, 2023 may claim the credit on their tax return based on the updated vehicle classification definition provided in Notice 2023-16 issued on Feb. 3, 2023, and incorporated in the April 2023 proposed regulationsPDF, and the associated MSRP limitation. All vehicles that were classified as an SUV, van or pickup truck for the purpose of the New Clean Vehicle Tax Credit prior to the updated notice continue to be subject to the same $80,000 MSRP limitation. Some vehicles that were previously subject to the $55,000 MSRP limitation are now classified as SUVs and therefore get the benefit of the $80,000 MSRP limitation. The vehicles now classified as SUVs for this purpose include but may not be limited to the 2023 Cadillac Lyriq, the 2022 and 2023 Ford Mustang Mach-E, certain variants of the 2022 and 2023 Tesla Model Y, certain variants of the 2022 and 2023 Volkswagen ID.4, and the 2022 and 2023 Ford Escape Plug-In Hybrid. In the case where vehicles have been reclassified for the purpose of this credit, taxpayers should obtain a report from the seller: See Topic B FAQ 9. Vehicles placed in service on or after April 18, 2023, must also meet the critical minerals and battery sourcing requirements to claim the credit.

Q9. What information does a seller have to provide to a taxpayer purchasing a new clean vehicle to allow the taxpayer toclaim the New Clean Vehicle Credit? (updated Oct. 6, 2023)

A9. A seller must provide the following information on a report to the taxpayer and to the IRS ("seller report" or "time of sale report"):

- Name and taxpayer identification number of the seller.

- Name and taxpayer identification number of the taxpayer (only one taxpayer may be listed on the seller report; in the event of multiple owners, only the taxpayer that intends to claim the credit should be listed).

- Vehicle identification number (VIN) of the new clean vehicle.

- Battery capacity of the new clean vehicle.

- Verification that the taxpayer is the original user of the new clean vehicle.

- The date of the sale and the sale price of the vehicle.

- Maximum credit allowable for the new clean vehicle being sold.

- For sales after December 31, 2023, the amount of any transfer credit applied to the purchase.

- A declaration under penalties of perjury from the seller.

For further details see Revenue Procedure 2022-42 and Revenue Procedure 2023-33PDF.

Q10. When must the seller provide the report to the taxpayer? (updated Oct. 6, 2023)

A10. The seller must provide the report to the taxpayer not later than the date the vehicle is purchased. However, taxpayers that did not receive a report from the seller because their vehicle was previously ineligible but their vehicle is now eligible (such as due to a change in the vehicle's classification and the applicable MSRP limitation) may request and receive a report from the seller after the vehicle's purchase date.

For further details see Revenue Procedure 2022-42 and Revenue Procedure 2023-33PDF.

Q11. How will a seller provide these reports to the IRS? (updated April 16, 2024)

A11. For vehicle sales occurring in calendar year 2023, sellers must file reports by Feb. 15, 2024, by fax. For vehicle sales occurring in calendar year 2024 and later, sellers must file reports within 3 days of the time of sale through IRS Energy Credits Online. For further details see Revenue Procedure 2022-42, Revenue Procedure 2023-33PDF and Revenue Procedure 2024-12.