The Electric Vehicle Experience Insights from Real World EV Owners

McKinsey Electric Vehicle Index: Europe cushions a global plunge in EV sales

McKinseys proprietary Electric Vehicle Index (EVI) assesses the dynamics of the e-mobility market in 15 key countries worldwide (for more information on the metrics evaluated, see sidebar What is the Electric Vehicle Index?). EVI results for 2019 and the first quarter of 2020 provide important insights about market growth, regional demand patterns, market share for major electric-vehicle (EV) manufacturers, and supply-chain trends.

Growth in the electric-vehicle market has slowed

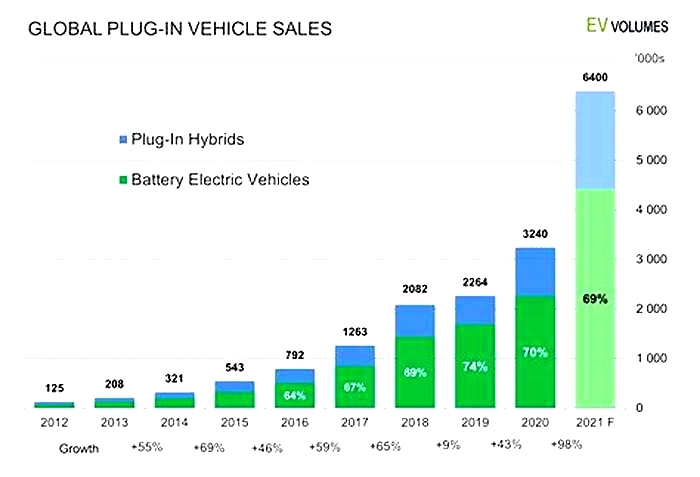

EV sales rose 65 percent from 2017 to 2018 (Exhibit 1). But in 2019, the number of units sold increased only to 2.3 million, from 2.1 million, for year-on-year growth of just 9 percent. Equally sobering, EV sales declined by 25 percent during the first quarter of 2020. The days of rapid expansion have ceasedor at least paused temporarily. Overall, Europe has seen the strongest growth in EVs.

Although these developments are disappointing, they largely reflect the decline of the overall light-vehicle market, which fell by 5 percent in 2019 and by an additional 29 percent in first-quarter 2020. Despite the overall drop in sales, global EV market penetration increased by 0.3 percentage points from 2018 to 2019, for a total share of 2.5 percent. With additional growth in the first quarter of 2020, EV penetration is now at 2.8 percent.

To gain different perspectives on the EV industrys growth and other topics, we interviewed various McKinsey experts (see sidebar, Expert views on the electric-vehicle sectors future development). The remainder of this section explores regional market variations.

EV market trends vary by region

Key EV markets suggest shifting regional dynamics, with China and the United States losing ground to Europe. EV sales remained constant in China in 2019, at around 1.2 million units sold (a 3 percent increase from the previous year). In the United States, EV sales dropped by 12 percent in 2019, with only 320,000 units sold. Meanwhile, sales in Europe rose by 44 percent, to reach 590,000 units. These trends continued in first-quarter 2020 as EV sales decreased from the previous quarter by 57 percent in China and by 33 percent in the United States. In contrast, Europes EV market increased by 25 percent.

Key EV markets suggest shifting regional dynamics, with China and the United States losing ground to Europe.

China

The relatively slow 2019 growth of Chinas EV market reflects both an overall decline in the light-vehicle market and significant cuts in EV subsidies. The central government, for example, eliminated purchase subsidies for vehicles that achieve electric ranges (e-ranges) of less than 200 kilometers and reduced subsidies by 67 percent for battery electric vehicles (BEVs) with e-ranges above 400 kilometers. These cutbacks reflect the governments strategy of scaling back monetary incentives for new-energy vehicles (NEVs) and transitioning to nonmonetary forms of support. Since 2019, OEMs have received credits for each NEV produced. The credits take into consideration factors such as the type of vehicle, as well as its maximum speed, energy consumption, weight, and range. Regulators base credit targets for each OEM on its total production of passenger cars. If a manufacturer does not reach the target, it must purchase credits from competitors that have a surplus or pay financial penalties.

In first-quarter 2020, China was heavily affected by the COVID-19 pandemic. EV sales dropped by 57 percent from the fourth quarter of 2019 as consumer demand declined sharply. Several EV manufacturers were also forced to halt production. In response, the central government extended through 2022 (though at reduced rates) monetary incentives that were about to expire. The government also prolonged the purchase-tax exemptions of NEVs through 2022. These measures, together with the governments recent decision to invest billions of renminbi in the charging infrastructureas part of an economic-stimulus program, could help EV sales rebound in 2020.

The United States

EV sales rose by 80 percent in the United States in 2018, driven by the market launch of the standard version of the Tesla Model 3. The increase slowed in 2019 because of several developments. With Teslas overseas deliveries increasing and the gradual phaseout of the federal tax credit in January and July 2019, the brands US sales for that year declined 7 percent, or 12,400 units. Meanwhile, the Chevrolet Volt was phased out, and its sales fell by 14,000 units. Sales of the Honda Clarity also decreased by 8,000 units.

Some international OEMs did successfully launch new models in the United States in 2019, including Audi (the e-tron) and Hyundai (the Kona). Sales of VWs e-Golf also increased. These three brands accounted for more than 24,500 units of EV sales, but their strong performance could not offset the decline of other models. US sales of EVs decreased further in first-quarter 2020, by 33 percent from the previous quarter.

The federal governments recent moves to loosen regulations could further decelerate the EV market in the United States. In March 2020, for instance, the government revised fuel-economy standards, to a 2026 target of 40 miles per gallon (mpg), from 54 mpg. Todays low oil prices are also contributing to the EV slowdown, since they significantly lower the total cost of ownership for vehicles powered by internal-combustion engines (as compared with EVs). These changes are creating great uncertainty, and the US EV markets development could depend largely on the number of states adopting Californias Zero-Emission Vehicle Program and on the vicissitudes of oil prices.

Europe

Unlike other key EV markets, Europe has seen significant EV growth. In 2019, sales increased by 44 percent, the highest rate since 2016. The European Unions new emissions standard95 grams of carbon dioxide per kilometer for passenger carscould also boost EV sales because it stipulates that 95 percent of the fleet must meet this standard in 2020 and 100 percent in 2021. BEV sales picked up speed substantially, with a 70 percent growth rate propelled by three models: the Tesla Model 3, Hyundai Kona, and Audi e-tron.

EV sales increased by double-digit percentages in 2019 in almost every European country. Sales in some smaller markets, such as Estonia, Iceland, and Slovakia, declined in absolute terms. EV sales in Germanyand the Netherlands contributed nearly half44 percentof overall EV-market growth in Europe; in both countries, units sold increased by about 40,000 units. Those numbers translate into a 2018 growth rate of 55 percent for Germany and 144 percent for the Netherlands. In both countries, these strong EV sales resulted from increased demandfor new models, the availability of existing models with larger battery sizes, and changed government incentives (for more information on the power of incentives, see sidebar Purchase subsidies juice EV sales.)

In the first quarter of 2020, European EV sales rose as the overall EV penetration rate increased to 7.5 percent. With the exception of Hong Kong, all of the top ten markets for EV penetration were in Europe (Exhibit 2). The strong regulatory tailwinds and high purchase incentives in several European countries could dampen the impact of the COVID-19 pandemic and further boost the EV market. That said, EV sales will probably face tougher impediments in second-quarter 2020, when the pandemics impact on Europes countries and economies should peak. So far, no European OEM has changed its plans to roll out EV models, and several countries are discussing additional purchase incentives as part of their economic-stimulus programs.

Electric-vehicle makers are debuting new models and boosting sales of existing ones

Automakers launched 143 new electric vehicles105 BEVs and 38 plug-in hybrid electric vehicles (PHEVs)in 2019. They plan to introduce around 450 additional models by 2022 (Exhibit 3). Most are midsize or large vehicles. Given the estimated production levels, German manufacturers, with an expected volume of 856,000 EVs, could overtake Chinese players in 2020. That would boost Germanys global production share from 18 percent in 2019 to 27 percent in 2020.

New emissions regulations in Europe and China, which will come into force between 2020 and 2021, partly explain why EV-model launches have increased significantly. These regulations pose major challenges for automakers, since they will face potential penalties of up to several billion euros unless they increase their EV penetration rates significantly.

Among EV manufacturers, Tesla continued as market leader in 2019, with 370,000 units sold globally, for a market share of about 16 percent, up from 12 percent in 2018 (Exhibit 4). The launch of the Model 3 outside of the United States was the main reason for this surge. With 300,000 units sold worldwide, the Model 3 outpaced sales of the BJEV EU-series threefold and sales of Nissan Leaf fourfold.

At the brand level, most Chinese EV manufacturers faced declining sales, while demand was high for the EV offerings of some international OEMs.

The supply chain is localizing

With announced launches of new EV models spiking, both automakers and suppliers are increasing their global footprints in target markets by localizing the production of vehicles and components. For example, Tesla began construction of its Shanghai plant in January 2019 and delivered the first locally produced EV that December. The company plans to build its next production plant in Germany by 2021. Similarly, Volkswagen and Toyota have announced plans to set up EV plants in China.

In a similar development, battery-cell manufacturers are increasing their production capacities in target markets. The total lithium-ionbattery market for EV passenger cars grew by 17 percent, to 117 gigawatt-hours in 2019, enough to power 2.4 million standard BEVs. Most of the new capacity will be established in Central Europe, with companies preparing to meet demand throughout the region. Company announcements suggest that the global market should expand to about 1,000 gigawatt-hours by 2025. The Chinese battery maker CATL had the largest market share in 2019, at 28 percent, while its absolute capacity grew by 39 percent. CATL has recently continued its global expansion, signing new contracts with several international OEMs and setting up a factory in Germany.

South Korean manufacturers are trying to catch up with large-scale investments in new overseas production plants. SK Innovation, for example, announced it would invest an additional 5 billion in its planned US factory, while LG Chem is investing $2.3 billion in a joint venture (JV) with General Motors in the United States.

Overall, JVs are becoming a popular collaboration model in the battery industry, with an increasing number of partnerships announced in 2019. This trend mainly reflects the fact that JVs enable automakers to lock in enough capacity to reach their ambitious sales and production targets. Automakers also prefer multisourcing strategies involving a number of cell makers. Even Tesla, which used to rely solely on cells from Panasonic, signed new contracts with CATL and LG Chem for the Chinese market in 2019.

The EV market has grown quickly, but the dynamics vary by region. In key markets, the transition from ICEs to electric powertrains reached a tipping point in 2019, fueled by more stringent emissions regulations, access restrictions in cities, advancing EV technologies that lengthen driving ranges and cut prices, and the expansion of the charging network. The same forces will further expand uptake over the coming years, but their evolution will vary by market.

To win, automakers and suppliers must develop a detailed view of whats happening in each market by monitoring the regulatory environment, customer preferences, infrastructure development, and the moves of competitorsespecially new entrants, including start-ups from outside the industry. Companies that match customer demand with suitable EV models and catch regulatory tailwinds may secure the most promising pockets of growth going forward.

Global

After a decade of rapid growth, in 2020 the global electric car stock hit the 10million mark, a 43% increase over 2019, and representing a 1% stock share. Battery electric vehicles (BEVs) accounted for two-thirds of new electric car registrations and two-thirds of the stock in 2020. China, with 4.5 million electric cars, has the largest fleet, though in 2020 Europe had the largest annual increase to reach 3.2million.

Overall the global market for all types of cars was significantly affected by the economic repercussions of the Covid-19 pandemic. The first part of 2020 saw new car registrations drop about one-third from the preceding year. This was partially offset by stronger activity in the second-half, resulting in a 16% drop overall year-on-year. Notably, with conventional and overall new car registrations falling, global electric car sales share rose 70% to a record 4.6% in 2020.

About 3million new electric cars were registered in 2020. For the first time, Europe led with 1.4 million new registrations. China followed with 1.2 million registrations and the United States registered295000 new electric cars.

Numerous factors contributed to increased electric car registrations in 2020. Notably, electric cars are gradually becoming more competitive in some countries on a total cost of ownership basis. Several governments provided or extended fiscal incentives that buffered electric car purchases from the downturn in car markets.

Europe

Overall Europes car market contracted 22% in 2020. Yet, new electric car registrations more than doubled to 1.4million representing a sales share of 10%. In the large markets, Germany registered 395000new electric cars and France registered 185000. The United Kingdom more than doubled registrations to reach 176000. Electric cars in Norway reached a record high sales share of 75%, up about one-third from 2019. Sales shares of electric cars exceeded 50% in Iceland, 30% in Sweden and reached 25% in the Netherlands.

This surge in electric car registrations in Europe despite the economic slump reflect two policy measures. First, 2020 was the target year for the European Unions CO2 emissions standards that limit the average carbon dioxide (CO2) emissions per kilometre driven for new cars. Second, many European governments increased subsidy schemes for EVs as part of stimulus packages to counter the effects of the pandemic.

In European countries, BEV registrations accounted for 54% of electric car registrations in 2020, continuing to exceed those of plug-in hybrid electric vehicles (PHEVs). However, the BEV registration level doubled from the previous year while the PHEV level thripled. The share of BEVs was particularly high in the Netherlands (82% of all electric car registrations), Norway (73%), United Kingdom (62%) and France (60%).

China

The overall car market in China was impacted by the panademic less than other regions. Total new car registrations were down about 9%.

Registration of new electric cars was lower than the overall car market in the first-half of 2020. This trend reversed in the second-halfas China constrained the panademic. The result was a sales share of 5.7%, up from 4.8% in 2019. BEVs were about 80% of new electric cars registered.

Key policy actions muted the incentives for the electric car market in China. Purchase subsidies were initially due to expire at the end of 2020, but following signals that they would be phased out more gradually prior to the pandemic, by April 2020 and in the midst of the pandemic, they were instead cut by 10% and exended through 2022. Reflecting economic concerns related to the pandemic, several cities relaxed car licence policies, allowing for more internal combustion engines vehicles to be registered to support local car industries.

United States

The US car market declined 23% in 2020, though electric car registrations fell less than the overall market. In 2020, 295000new electric cars were registered, of which about 78% were BEVs, down from 327000 in 2019. Their sales share nudged up to 2%. Federal incentives decreased in 2020 due to the federal tax credits for Tesla and General Motors, which account for the majority of electric car registrations, reaching their limit.

Other countries

Electric car markets in other countries were resilent in 2020. For example, in Canada the new car market shrunk 21% while new electric car registrations were broadly unchanged from the previous year at 51000.

New Zealand is a notable exception. In spite of its strong pandemic response, it saw a decline of 22% in new electric car registrations in 2020, in line with a car market decline of 21%. The decline seems to be largely related to exceptionally low EV registrations in April 2020 when New Zealand was in lockdown.

Another exception is Japan, where the overall new car market contracted 11% from the 2019 level while electric car registrations declined 25% in 2020.Theelectric car market in Japan has fallen in absolute and relative terms every year since 2017, when it peaked at 54000registrations and a 1% sales share. In 2020, there were 29000registrations and a 0.6% sales share.